Posting this one for all subs - both free and paid.

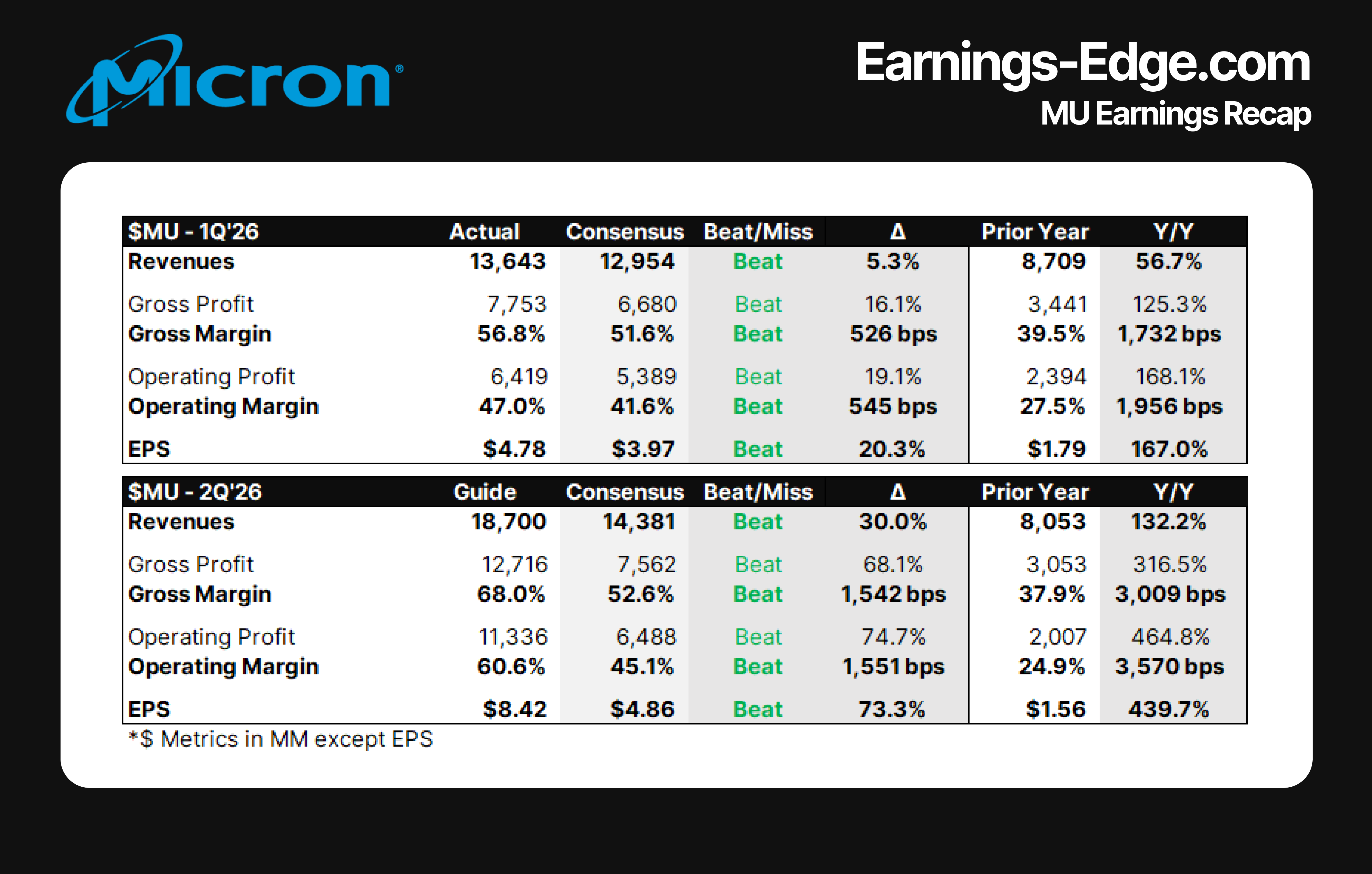

Check out the level of upside both in Micron’s 1Q and how that accelerates into the 2Q guidance:

30% revenue upside and 1,500bps+ of margin excess with nearly 75% of EPS upside. It’s safe to say that the forward earnings revisions accelerated again from 12% two quarters ago to 20% last quarter and even further as we look ahead.

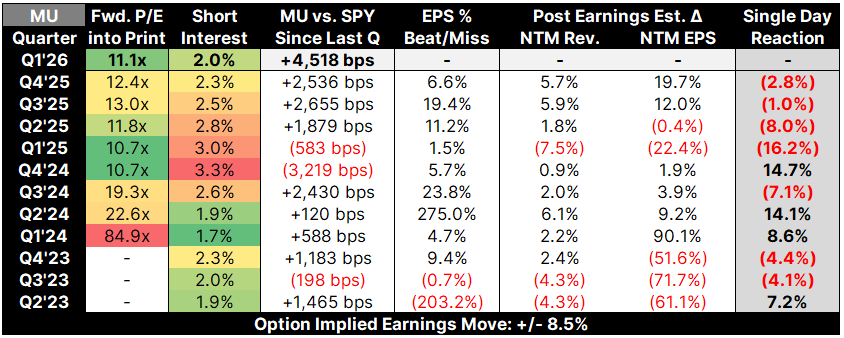

Here’s the historical context, and we note (as we did in our preview) that the multiple actually CONTRACTED into the print as analysts chased memory price increases:

Shares +7%, but still lower than we began the week…

https://open.substack.com/pub/techitalt/p/my-take-on-micron-mu?r=5jmutn&utm_campaign=post&utm_medium=web&showWelcomeOnShare=true