The Biggest Week: Consensus Estimates and Setups for Google, Apple, Microsoft, Amazon, Meta, SanDisk, Western Digital, Seagate, and Qualcomm

Your Guide for Benchmarking Earnings from this Week's Biggest Names

Tinkering with a new format this week by including Consensus expectations in this preview post. Curious to hear your feedback!

Relative Winners and Losers

Google / Alphabet (GOOGL)

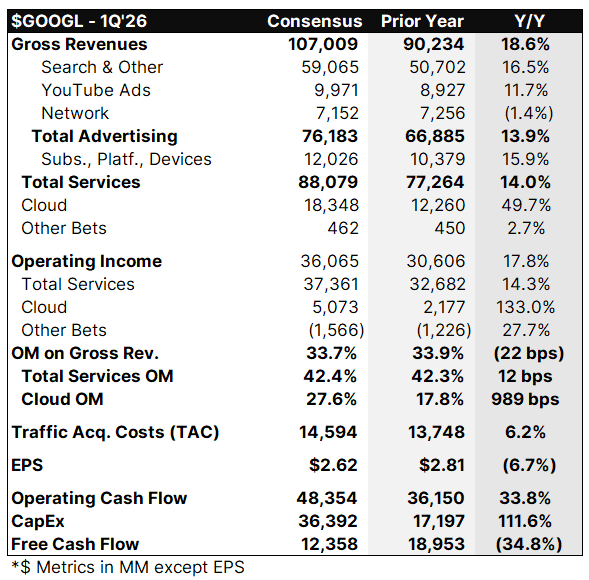

Consensus estimates for the quarter and forward periods:

Bull Bullets: Gemini Scale, Cloud Inflection, and Antitrust Clarity Fuel Re-Rating Potential

Gemini’s 750M+ monthly active users and 16 billion tokens processed per minute via direct API use position Alphabet to monetize AI at a scale no other company can match, with Gemini Enterprise paid users growing 40% quarter-over-quarter in Q1 and enterprise pricing at $42-62 per million tokens creating a multi-billion-dollar incremental revenue stream if adoption targets are met. The Wiz acquisition, completed in March, could add $300M-$400M to Q2 cloud growth and strengthens Google’s security-as-a-service moat in the enterprise market.

Google Cloud’s $70B+ annual run rate and $155B backlog, combined with 75% of Cloud customers already using AI products, suggest the business is crossing from “growth investment” into a durable, high-margin profit center. With just over half of the planned $175B-$185B in 2026 CapEx directed toward Cloud infrastructure, Alphabet is making its largest-ever bet that enterprise AI demand is structural, not cyclical, and the Apple-Siri partnership using Gemini models adds a powerful new distribution channel.

The September 2025 antitrust remedies ruling rejected forced Chrome divestiture and AI investment caps, removing the worst-case regulatory overhang. While the DOJ’s cross-appeal continues, Wedbush characterized the outcome as removing “lingering risks associated with the worst-case outcome,” and at roughly 29x forward earnings, Alphabet still trades at a discount to mega-cap peers despite best-in-class margins and faster earnings growth.

Bear Bullets: Massive CapEx Commitment, Search Disruption Risk, and Ongoing Legal Uncertainty

The $175B-$185B CapEx guidance for 2026 represents a potential doubling from 2025 levels, and if Cloud growth decelerates or AI monetization disappoints, that spending transforms from a growth investment into margin compression. Investors need to see clear evidence that infrastructure spend is converting backlog into recognized revenue, and any sign of capacity oversupply would pressure the multiple quickly.

Alphabet itself flagged new AI-related risks in its latest filings, acknowledging that generative AI adoption could cause consumers to decrease internet search usage and that there is “no assurance” it will adapt advertising formats effectively. ChatGPT’s 800M weekly active user base and the emerging risk that a competitor perfects AI-native search monetization faster than Google represent a real threat to the core advertising engine that still drives the majority of revenue.

The DOJ’s cross-appeal seeking Chrome divestiture and mandatory choice screens heads to the D.C. Circuit in late 2026 or early 2027, keeping structural remedy risk alive. Morgan Stanley analysts estimated that mandatory choice screens alone could cost Google 5-8% of search traffic over three years, translating to $15-25B in annual advertising revenue at risk, and the data-sharing requirements from the existing ruling could strengthen competitors over a five-year window.

Key Investment Thesis

Alphabet is a global technology conglomerate operating the world’s dominant search engine, the fastest-growing major cloud platform, and the YouTube video ecosystem.

Upside Case: If Cloud sustains 40%+ growth while Gemini monetization accelerates across enterprise, search, and the new Apple partnership, Alphabet could see multiple expansion from 29x toward the 32-35x range its mega-cap peers command, translating to price targets in the $370-$430 range as AI spending converts to visible margin improvement.

Downside Case: If AI spending balloons without proportional revenue conversion, or if the DOJ appeal results in Chrome divestiture or punitive choice screens, the combination of margin pressure and search traffic erosion could compress the multiple below 25x and push shares toward the low $200s.

Differentiation: Alphabet is the only company with a dominant position in search advertising, a top-three cloud platform, a leading AI model family (Gemini), custom AI silicon (TPUs), and the world’s largest video platform, giving it more levers to monetize AI than any single competitor.

Apple (AAPL)

Consensus estimates for the quarter and forward periods: