I have been thinking about ways to improve my daily Setup posts, and I want to seek your feedback about how useful these changes would be. Additionally, if you have suggestions for other additions/changes, I would love to hear them.

First, a few changes to the data within the tables:

Adding next twelve months’ EPS/revenue growth: This would contextualize either the price-to-earnings/price-to-sales ratios. Does near-term growth match the multiple?

Adding a ‘multiple premium/discount’ column: This would track the relative performance of a company’s multiple vs. the aggregate SPY multiple over time. Maybe now Microsoft is 20x forward earnings vs. SPY 18x forward earnings, but last quarter Microsoft was 25x and SPY was 15x. This better contextualizes a given multiple for the user.

Second, written contextualization of the Setup table, and three bullet points each for the Bull and Bear narratives for each company.

Here’s the ‘Names of Note’ piece I just shared, rewritten with these additions. Yes, this leans heavily into AI, and this is a quick-and-dirty first take that I will improve with better models, better prompts, and improved linguistic style. Please consider the format / approach more so than the content detail.

Broadcom (AVGO)

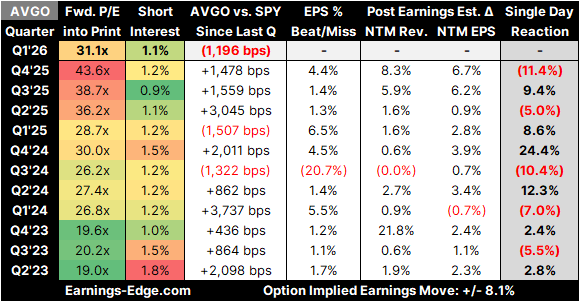

📊 Synopsis

Broadcom has been an AI infrastructure powerhouse, growing from a ~27x forward P/E in early 2024 to a peak near 44x in Q4’25 before normalizing back to the low 30s. The stock has generally outperformed SPY across most recent quarters — note the frequent positive ‘vs. SPY’ readings. Post-earnings reactions have been volatile, with a painful -11.4% in Q4’25 driven by margin compression concerns despite a revenue beat. EPS beats have been consistent and strong, though NTM estimates moved modestly. The options market prices in ±8.1% for Q1’26, and analysts remain strongly bullish into the March 4 earnings report.

🐂 Bull Case

• Custom AI ASIC dominance: Broadcom’s hyperscaler AI chip partnerships (Google, Meta, Apple, Microsoft) are generating $50B+ in projected AI revenue for 2026 — a massive, durable moat as cloud giants prioritize proprietary silicon over off-the-shelf GPUs.

• VMware flywheel fully spinning: The $69B acquisition has integrated ahead of schedule, converting VMware’s perpetual license base into high-margin recurring software revenue that now accounts for ~25% of total revenue with minimal incremental cost.

• Valuation reset creates entry: After correcting from ~$415 ATHs to ~$330, AVGO trades at a more reasonable ~31x forward P/E for a business growing revenue 28%+ YoY with 68% EBITDA margins — an attractive risk/reward that JPMorgan named a top semiconductor pick.

🐻 Bear Case

• Margin compression is real: Management flagged near-term gross margin pressure due to hardware mix shift (AI chips carry lower margins than software), alongside a 2026 tax rate increase — the exact combination that caused the -11% post-earnings collapse in December.

• China export risk and customer concentration: A meaningful portion of AVGO’s chip revenue is exposed to geopolitical risk from U.S.-China trade tensions, while hyperscaler customer concentration means a single contract loss or budget shift could materially dent AI revenue.

Premium valuation leaves no room for error: At ~31x forward earnings and ~15x sales on AI-elevated expectations, any miss or guidance reduction — particularly around AI custom chip ramp timelines — risks multiple contraction in a market already sensitive to tech valuations.

Alibaba Group Holding (BABA)