Retailer Bonanza: Complete Earnings Coverage for Walmart, Target, Home Depot, Lowe's, TJ Maxx, Williams Sonoma, Ralph Lauren, Deckers, and Many More

Earnings Estimates, Valuation Context, and Bull / Bear Debate for the Week's Retailers

This week we kick-off retailer earnings with almost all of the heavy hitters: Walmart, Target, Home Depot, Lowe’s, TJ Maxx, and many more. This post provides Consensus expectations, historical valuation context, and bull-bear debate for each.

Before getting into individual company analysis, let’s look at the outperformers and underperformers over the last three months (funny enough there are NO outperformers relative to the SPY):

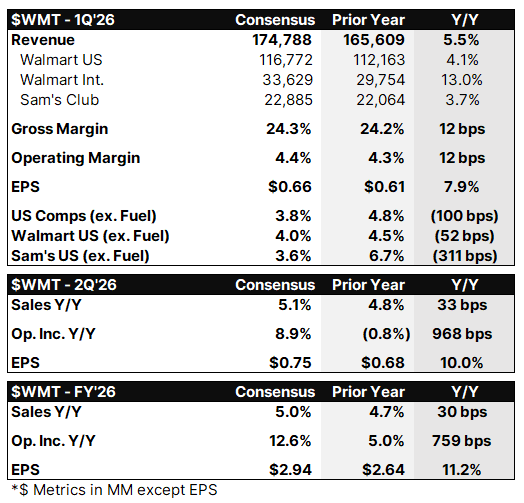

Walmart (WMT)

Bull Bullets: New CEO debut unlocks AI, automation, and capital-return inflection

John Furner’s first earnings call as CEO on May 21 represents a strategic reset moment, with management already signaling that automation, mix shift, and AI-driven productivity will be the FY27 margin levers. The recent decision to relocate or eliminate roughly 1,000 corporate roles in an AI efficiency push provides early evidence that cost discipline will accompany the leadership change.

The newly authorized $30 billion share repurchase program and FY27 guidance for operating income growth of 6 to 8 percent (versus sales growth of 3.5 to 4.5 percent) point to a multi-year operating leverage story, supported by capex peaking at roughly 3.5 percent of sales as the automation buildout matures. Free cash flow growth of 18 percent in FY26 sets up meaningful incremental buyback capacity through FY27 and FY28.

High-margin advertising (Walmart Connect), Walmart+ membership economics, and continued international e-commerce strength (24 percent global e-commerce growth last quarter) are reshaping the revenue mix toward structurally higher-margin streams. As these scale alongside tariff cost moderation in the back half of FY27, gross margin and operating margin can decouple from low-single-digit comp growth.

Bear Bullets: Leadership change, tariff pass-through, and rich valuation cap upside

Two simultaneous leadership transitions, with Furner replacing Doug McMillon and Walmart International CEO Kath McLay also departing, introduce execution risk during a tariff-heavy operating environment. Furner has explicitly framed FY27 guidance as conservative, raising the risk of a disappointing tone if early macro indicators soften.

Walmart remains the largest US importer of consumer goods, and management has acknowledged ongoing “peak tariff-related impacts” pressuring grocery and health and wellness mix. A strategy of absorbing costs to defend price leadership leaves margin guidance dependent on tariff de-escalation that is not yet visible.

With shares around $130 and the median analyst price target at roughly $130 to $138, the stock prices in much of the bull case already. The P/E gap versus Costco has narrowed, and any deceleration in e-commerce or hint of Sam’s Club membership friction could trigger a meaningful multiple reset given the defensive premium.

Key Investment Thesis

Walmart is the world’s largest omnichannel retailer, operating about 10,900 stores in 19 countries with a rapidly scaling e-commerce, advertising, and membership stack.

Upside Case: New CEO Furner extends Walmart’s hybrid retail leadership while automation, advertising, and membership compound margin expansion above 8 percent operating income growth, supporting mid-teens total shareholder returns through buybacks and dividend growth.

Downside Case: Tariff costs prove stickier than guided, the CEO transition produces an operational stumble, and consumer trade-down momentum stalls as competitors close the digital gap, compressing the premium multiple toward historical averages.

Differentiation: Walmart’s scale advantage in grocery (roughly 60 percent of US sales), its first-party advertising business, and its integrated supply chain technology stack create a defensive moat that pure e-commerce or specialty competitors cannot replicate.

Target (TGT)