As we previewed, Lennar posted a weak set of 3Q results that set the stage for a soft 4Q and leave investors in hope that rate relief can resuscitate the new construction market.

The one bright spot here is the lack of a collapse in orders (beating by 2.5% in the quarter), but those fail to translate in the near term, with the 4Q home delivery outlook falling a whopping 12% short of expectations.

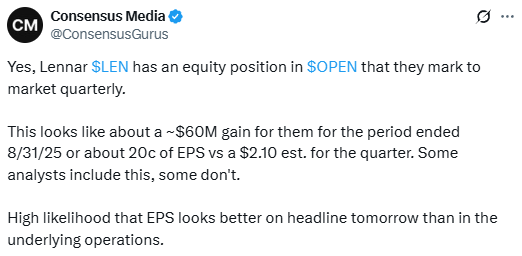

The headline EPS ‘beat’ seems to be supporting the stock here initially, but that beat results from a non-operational gain in the company’s mark-to-market equity investments (29c of EPS benefit in the quarter; 20c from Opendoor). We discussed this on Twitter:

Our EPS comparison below strips out this gain for an apples to apples comparison: