Earnings Edge for Wednesday: Setups for Uber, AppLovin, Arm Holdings, Disney, DoorDash, Coherent, Dutch Bros, Axon, and 100+ More

Relative winners and losers over the last quarter, followed by names of note, concluding with a spreadsheet containing setup tables for all of the day’s reporters.

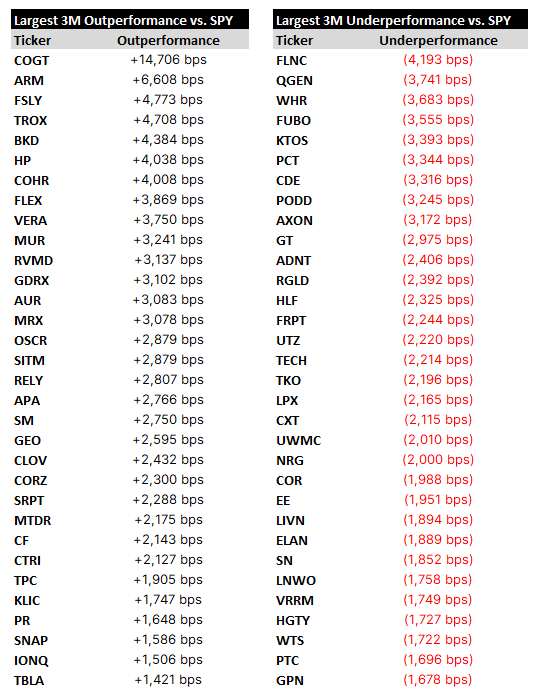

Relative Winners and Losers

Names of Note

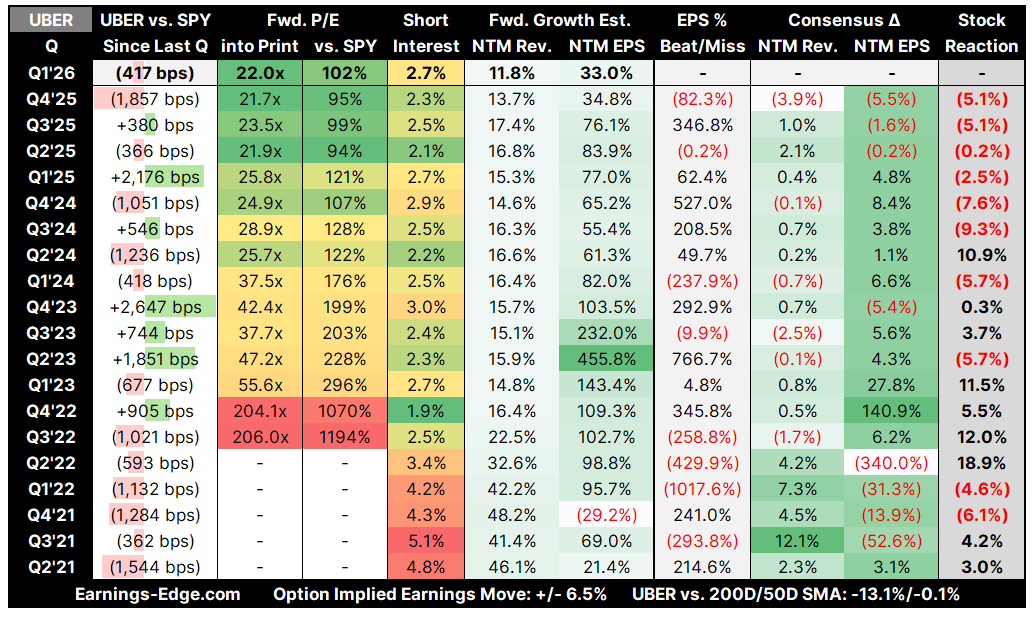

Uber Technologies (UBER)

Bull Bullets: $10B AV Commitment, Platform Dominance, and Buyback Firepower Position Uber for Re-Rating

Uber’s $10 billion-plus commitment to autonomous vehicles, split between $2.5B in equity stakes (Lucid, WeRide, Nuro, Wayve, Rivian) and $7.5B in robotaxi fleet purchases, transforms its narrative from “AV disruption victim” to the platform that mediates autonomous mobility globally. If initial Stellantis-supplied vehicles begin scaling toward the 100,000-unit target by 2027, Uber’s take rate on AV rides could be meaningfully higher than human-driven trips due to lower variable costs.

With operations in 10,000+ cities across 70 countries and over 450 million active users, Uber’s marketplace network creates a structural barrier that no AV-only competitor can replicate on its own. OEMs and AV developers are increasingly choosing to partner with Uber rather than build standalone consumer-facing ecosystems, as the cost of customer acquisition and fleet utilization optimization favors the platform model.

The $20 billion buyback authorization, combined with a stock trading at roughly 16x trailing earnings (below its 5-year median P/E of 18x), suggests the market has not fully priced in the durability of 17-21% constant-currency gross bookings growth. Adjusted EBITDA margins expanding from 3.9% to 4.5% of gross bookings indicate operating leverage that could compound meaningfully if the Trendyol Go integration and Delivery Hero stake increase deliver as planned.

Bear Bullets: AV Capex Risk, Asset-Heavy Pivot, and Competitive Disruption Threaten the Margin Story

The pivot from asset-light to owning or leasing $7.5B in robotaxi hardware represents a fundamental change to Uber’s capital structure, echoing its failed 2015-2018 moonshot era (Uber ATG, Uber Elevate, Jump). If autonomous technology milestones are not met and these vehicles sit underutilized, Uber absorbs depreciation and maintenance costs that could severely compress the free cash flow profile investors currently pay for.

Tesla’s Cybercab production is launching at Gigafactory Texas, and Waymo is targeting expansion to 20+ cities globally by late 2026 with a goal of 1 million weekly rides. Both competitors are pursuing vertically integrated strategies that could bypass Uber’s intermediary role entirely. If Tesla succeeds in building a direct-to-consumer robotaxi network, Uber’s platform premium erodes rapidly.

Q1 2026 consensus expects revenue near $13.3B, but Uber’s shares fell over 8% after its Q3 2025 report on soft EBITDA and margin guidance, showing the stock is highly sensitive to any forward guidance disappointment. The incoming CFO transition (Balaji Krishnamurthy replacing Prashanth Mahendra-Rajah) adds execution risk during a period requiring complex capital allocation across AV investments, buybacks, and international M&A.

Key Investment Thesis

Uber Technologies operates the world’s largest ride-hailing and delivery platform, connecting riders, eaters, and shippers with drivers and merchants in 70+ countries.

Upside Case: If Uber’s AV platform strategy succeeds in making it the demand aggregator for autonomous fleets from multiple OEM partners, the company effectively becomes the “Android of mobility,” earning a platform toll on every ride without bearing driver labor costs, potentially doubling or tripling per-trip margins over a multi-year horizon.

Downside Case: The $10B AV capital commitment could produce negative returns if technology timelines slip, regulatory approvals stall across key markets, or Tesla/Waymo build competing consumer networks that commoditize Uber’s marketplace advantage.

Differentiation: Uber is the only company simultaneously operating a 450M-user demand marketplace, running AV data collection fleets across dozens of cities, and providing end-to-end commercialization services (Uber Autonomous Solutions) to multiple competing AV developers.

AppLovin (APP)