Earnings Edge for Tuesday: Setups for AMD, Shopify, Lumentum, PayPal, Super Micro Computer, Ferrari, Arista Networks, Live Nation, Coupang, and Many More

Relative winners and losers over the last quarter, followed by names of note, concluding with a spreadsheet containing setup tables for all of the day’s reporters.

Relative Winners and Losers

Names of Note

Advanced Micro Devices (AMD)

Bull Bullets: Agentic AI CPU Demand and Hyperscaler Partnerships Drive Multi-Year Visibility

The structural shift from GPU-dominated pretraining toward inference and agentic AI workloads is reshaping the CPU-to-GPU ratio from 8:1 toward near parity, which positions AMD’s EPYC server CPU franchise for a demand inflection that the Street has only recently begun to underwrite. DA Davidson’s upgrade to Buy with a $375 target -- well above consensus of ~$290 -- reflects the view that Intel’s blowout Q1 signals a rising tide for AMD’s CPU business that estimates have not yet captured.

Multi-year commitments from OpenAI (6 GW deployment starting late 2026), Meta, and reportedly Anthropic for AMD’s upcoming MI450 GPU and Helios rack-scale platform provide revenue visibility extending through 2027 and beyond. The Samsung HBM4 memory supply agreement removes a key production bottleneck that previously constrained AMD’s AI accelerator shipment cadence, materially improving execution probability on large-scale deployments.

Analysts project roughly 60% EPS growth to $6.70 for calendar 2026, and that estimate has been trending upward as the data center demand picture clarifies. With the stock trading at ~33x 2027 earnings and a PEG ratio around 0.5, AMD offers a compelling growth-at-a-reasonable-price setup if MI450 customer wins convert at scale in H2.

Bear Bullets: Product Transition Gap, China Revenue Cliff, and NVIDIA Software Moat

AMD is navigating a product transition gap between current MI300-series shipments and the Helios platform (MI455X) expected in H2 2026. Q1 guidance of ~$9.8B implies a ~5% sequential revenue decline, and any delays in the Helios ramp would leave a meaningful hole in the data center revenue trajectory during the most competitively intense period in AI infrastructure.

The China revenue cliff is real: AMD guided MI308 sales to China at just ~$100M for Q1, down from a ~$390M windfall in late 2025 as U.S. export controls tighten further. This headwind is structural, not cyclical, and removes a revenue source that previously flattered growth rates.

NVIDIA’s CUDA software ecosystem remains the dominant standard in AI development, and ROCm still trails meaningfully despite forced optimization through AMD’s warrant structures with hyperscalers. If inference workloads prove more CUDA-dependent than bulls expect, AMD’s addressable market in AI accelerators could be more limited than the current multiple implies.

Key Investment Thesis

Advanced Micro Devices designs and sells high-performance CPUs, GPUs, and AI accelerators for data centers, PCs, and gaming.

Upside Case: The convergence of agentic AI workloads driving CPU demand toward GPU parity, combined with multi-year hyperscaler GPU commitments and the successful Helios platform launch in H2 2026, could drive AMD’s 35% revenue CAGR target and push earnings well above the current $6.70 consensus for 2026.

Downside Case: A product transition gap between current offerings and the Helios platform, ongoing China export restrictions, and the persistent CUDA software advantage could lead to disappointing near-term results and multiple compression from the current ~50x forward P/E.

Differentiation: AMD is the only company offering both leading-edge x86 CPUs and competitive AI GPUs in a single portfolio, enabling integrated CPU+GPU solutions that address the full stack of evolving AI workloads.

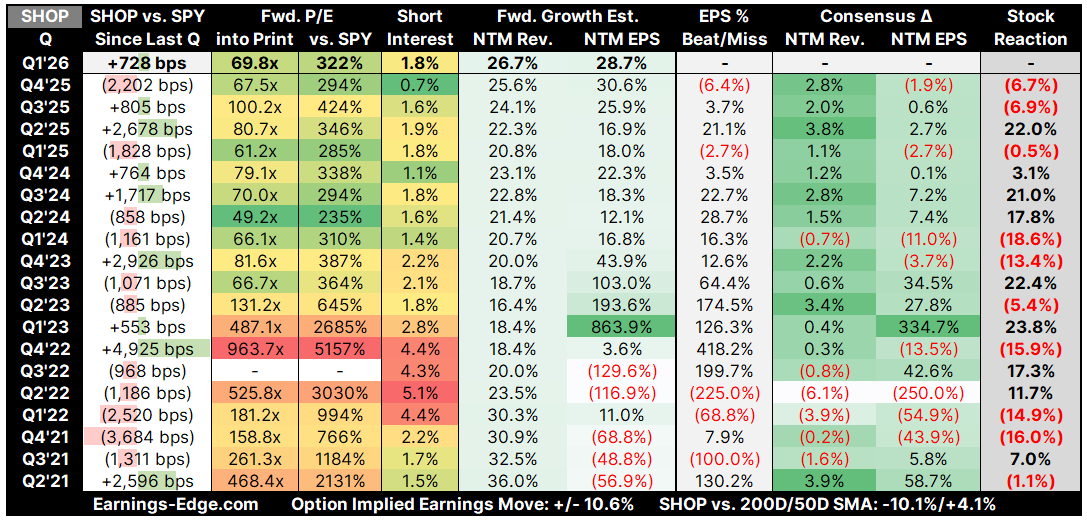

Shopify (SHOP)

Bull Bullets: Universal Commerce Protocol Positions Shopify as Infrastructure for Agentic Commerce