Earnings Edge for the Week Ahead: Setups for Netflix, ASML, Taiwan Semi, JPMorgan, Bank of America, Goldman Sachs, PepsiCo, CarMax, Charles Schwab, BlackRock, and Many More

Relative winners and losers over the last quarter, followed by names of note, concluding with a spreadsheet containing setup tables for all 60+ of the week’s reporters.

Relative Winners and Losers

Names of Note

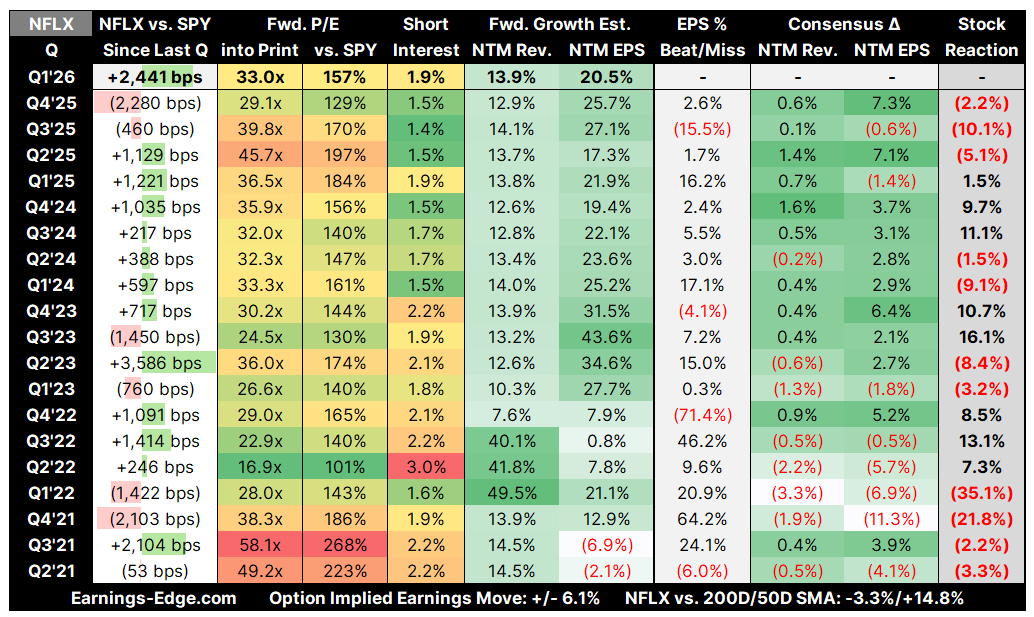

Netflix (NFLX)

Bull Bullets: Ad Revenue Doubling, WBD Exit Clarity, and Margin Expansion Fuel Re-Rating

Netflix’s advertising business more than doubled to ~$1.5B in 2025 and management has guided for it to roughly double again to ~$3B in 2026, representing a meaningful and still underappreciated revenue layer that carries structurally higher margins than subscription revenue — if this ramp materializes on schedule, consensus estimates may prove conservative.

The abandoned Warner Bros. Discovery bid — which Paramount Skydance ultimately won — removes a massive overhang: Netflix retains a $2.8B breakup fee, avoids billions in acquisition debt, and can now execute its organic growth roadmap with full capital flexibility, including an $8B remaining buyback authorization that could be deployed aggressively in 2026.

Live sports monetization (ad-supported viewers don’t skip ads and command premium CPMs) and a redesigned mobile interface planned for late 2026 are forward catalysts that the market has not fully priced in; Netflix management is guiding to $51B revenue and a 31.5% operating margin in 2026, reflecting continued operating leverage as content spend grows slower than revenue.

Bear Bullets: WBD Overhang Lingers, Content Cost Headwinds, and Valuation Leaves No Room for Error