Earnings Edge for the Week Ahead: Setups for Dell, Marvell, Salesforce, Snowflake, PDD Holdings, Zscaler, MongoDB, Okta, and 100+ More

Relative winners and losers over the last quarter, followed by names of note, concluding with a spreadsheet containing setup tables for all of the week’s reporters.

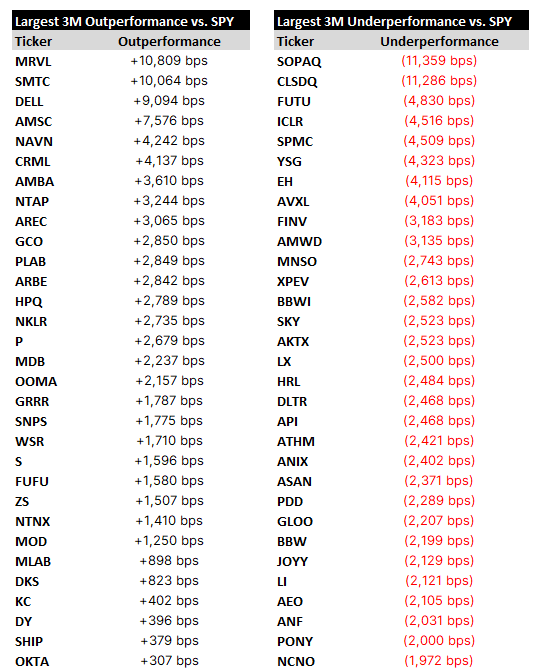

Relative Winners and Losers

Names of Note

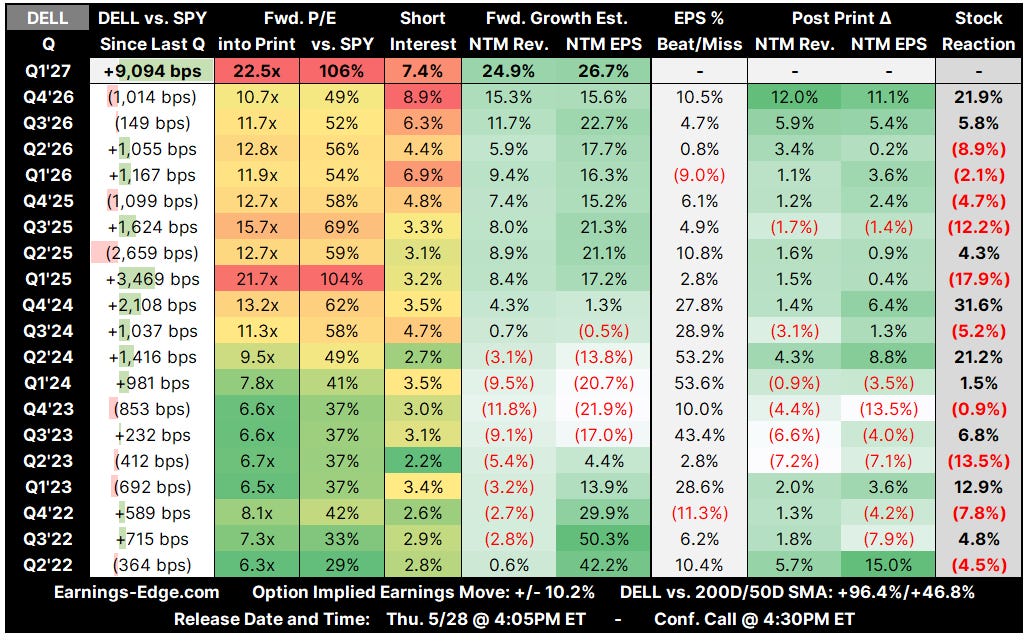

Dell Technologies (DELL)

Bull Bullets: $43B AI backlog converts into FY27’s $50B revenue ramp

The $43B AI server backlog entering FY27, combined with management’s $50B AI server revenue guide for the full year (roughly 100% growth), positions Dell as the primary winner in enterprise AI infrastructure capture. The May 28 print is the first checkpoint against the $13B Q1 AI revenue expectation, and any in-line or upside confirmation should sustain estimate revisions higher.

Recent Las Vegas product conference and broad analyst upgrades (JPMorgan to $280, Mizuho to $300) signal a structural re-rating thesis taking hold, where the market is starting to price the multi-year capex cycle rather than just one quarter of orders. Sovereign and enterprise customer breadth, with the customer count past 4,000, broadens the demand base beyond hyperscalers.

Potential Super Micro federal charge fallout (March 20) and persistent execution issues at peers could redirect an estimated $47B in displaced server demand toward Dell. As the highest-scale, vertically integrated rack provider with proven 500kW+ rack deployment capability, Dell is best positioned to absorb that share over the next twelve to eighteen months.

Bear Bullets: Memory cost cycle threatens to break margin leverage thesis

DRAM spot prices are up roughly 5.5x over six months, and Morgan Stanley’s underweight call sees FY27 gross and operating margins compressing 150-220bps with EPS down ~12% on a hardware-heavy mix. If Dell cannot reprice fast enough, the operating leverage story underpinning the EPS compounding thesis breaks.

AI-optimized server margins remain dilutive to corporate averages even as dollar margins grow, and CSG operating margins are already at the lower end of the long-term framework at 4.7%. PC demand is structurally muted with a shrinking unit market, leaving Dell increasingly dependent on a single, lower-margin AI revenue stream to drive the model.

The stock has rallied roughly 144% since the last earnings report and trades near 52-week highs, with options implying a +/-9.9% post-print move. The setup demands a clean beat-and-raise on both AI revenue and margins; anything less risks a sharp valuation reset, as UBS recently downgraded to Neutral citing the rally.

Key Investment Thesis Dell Technologies is a global infrastructure company selling AI-optimized servers, traditional servers, storage, networking, and PCs.

Upside Case: If Dell delivers the guided $13B in Q1 AI server revenue and reaffirms or raises the $50B FY27 AI target while stabilizing CSG margins through pricing actions, estimates revise higher and the multiple expands from ~14x forward toward levels reflecting the multi-year AI capex visibility. Continued backlog growth could reset the long-term revenue outlook above the 7-9% framework. Downside Case: Memory inflation accelerates faster than pricing can offset, compressing gross margins, while PC weakness and hyperscaler self-build pressure constrain growth. A backlog conversion miss or slower-than-expected enterprise broadening would crack the bull narrative tied to the $50B AI revenue path. Differentiation: Dell is the only OEM with both scale (over $19B ISG quarterly revenue) and proven rack-scale engineering for the highest-density AI deployments, with NVIDIA partnerships that few peers can match at this customer count.

Marvell Technology (MRVL)