Earnings Edge for Monday: Setups for AST SpaceMobile, Hims & Hers Health, Rigetti Computing, monday.com, Circle Internet, Figure Technology, Archer Aviation, Plug Power, ZoomInfo and Many More

Relative winners and losers over the last quarter, followed by names of note, concluding with a spreadsheet containing setup tables for all of the day’s reporters.

Relative Winners and Losers

Names of Note

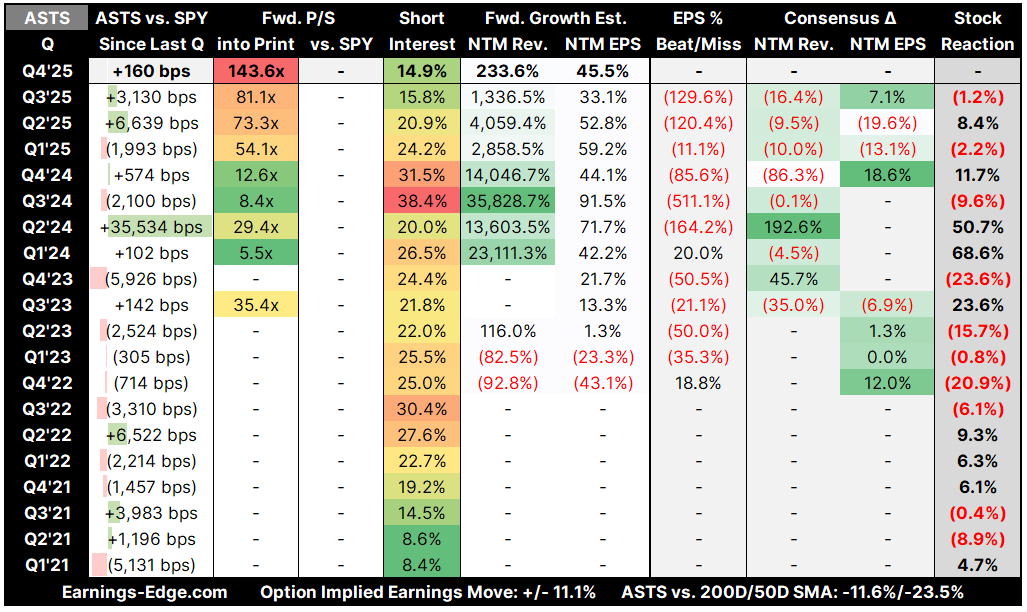

AST SpaceMobile (ASTS)

AST SpaceMobile is building the first space-based cellular broadband network designed to connect directly to standard, unmodified smartphones via a constellation of BlueBird satellites in low Earth orbit.

Bull Bullets: FCC Approval and MNO Partnerships Open Multi-Year Commercial Revenue Runway

FCC commercial authorization clears path to scaled operations. The April 22 grant allowing AST to deploy and operate up to 248 satellites removes the single largest U.S. regulatory gate, positioning the company to begin generating meaningful commercial service revenue through its AT&T, Verizon, and FirstNet partnerships as it scales toward its ~45-satellite year-end target.

Government and defense contracts diversify the revenue base early. The $30M Space Development Agency contract, combined with the stc Group prepayment and a growing pipeline of sovereign customer interest, provides near-term cash flow and validates the direct-to-device architecture for national security use cases that peers like Starlink are also chasing.

Expanding MNO partner network and institutional interest accelerate commercialization. The new Telus partnership (which included an equity stake), Google collaboration, and increasing institutional accumulation from names like Gotham Asset Management all signal broadening conviction in the business model ahead of meaningful revenue inflection in H2 2026.

Bear Bullets: Execution Delays and Cash Burn Pressure a Pre-Revenue Valuation

BlueBird 7 launch failure highlights binary execution risk. The Blue Origin upper-stage failure that effectively lost BlueBird 7 underscores how dependent ASTS’s timeline is on third-party launch providers; any further delays to the ~45-satellite year-end target could push commercial coverage windows into 2027 and compress the margin of error on cash runway.

Missed proxy milestones raise questions about management credibility. The February 2026 “number of satellites in orbit” milestone was marked as “Not Achieved” in the proxy filing, zeroing out that portion of CEO compensation and putting the market on alert for further schedule slippage at a moment when the stock trades at a rich multiple to negligible revenue.

Crowded competitive landscape from SpaceX, Globalstar, and Amazon. Starlink’s direct-to-cell service, Globalstar’s expanding LEO partnerships, and Amazon’s Project Kuiper all target similar connectivity gaps; if any of these well-capitalized rivals achieve commercial service first, ASTS’s first-mover narrative could erode rapidly.

Key Investment Thesis

Upside Case: If AST achieves its ~45-satellite orbit target by year end and begins generating commercial service revenue through its AT&T/Verizon/FirstNet partnerships in H2 2026, the company would validate a TAM that spans the billions of smartphones currently outside terrestrial coverage, potentially justifying a significant re-rating from its current pre-revenue valuation.

Downside Case: Continued launch provider failures, further satellite milestone misses, or accelerated progress from SpaceX or Amazon could push meaningful commercial revenue into 2027+, straining a balance sheet that relies on continued non-dilutive and dilutive capital raises to fund a capital-intensive satellite buildout.

Differentiation: ASTS is the only company with FCC authorization to deliver broadband-speed cellular service directly to unmodified consumer smartphones from space, a technical and regulatory moat that competitors have not yet replicated.

Hims & Hers Health (HIMS)