Buying and Selling Guide for Tuesday's Names of Note: CrowdStrike, Sea Ltd., Target, On Running, Best Buy, Sportradar, Thor, GitLab, Box, AutoZone, Ross Stores, and Many More

Relative winners and losers over the last quarter, followed by names of note, concluding with a spreadsheet containing setup tables for all of the day’s reporters.

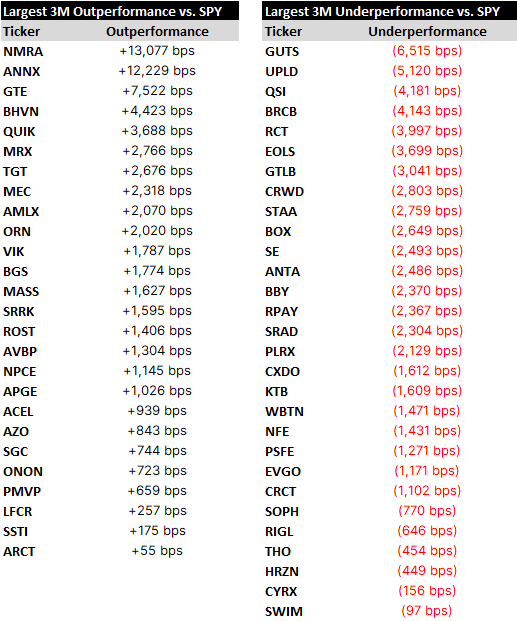

Relative Winners and Losers

Names of Note

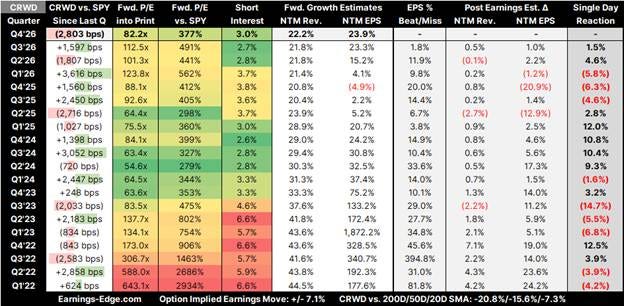

CrowdStrike (CRWD)

Bull Case

The platform consolidation thesis is playing out in real customer behavior: Falcon Flex ARR growing at triple digits means enterprises are actively expanding their relationship with CrowdStrike rather than switching to point solutions. That kind of net dollar retention is earned, not bought, and it creates a revenue durability that the table’s modest NTM EPS revision trend doesn’t fully capture.

The July 2024 outage turned out to be a test of the stickiness of mission-critical security software — and CrowdStrike passed. Customers with everything from endpoint protection to identity and cloud security running on one platform discovered they couldn’t easily switch mid-cycle. That lock-in is deeper than pre-outage bears feared.

AI is making the threat landscape more complex, not simpler, and CRWD is the only platform with the breadth of telemetry — trillions of events per week across millions of endpoints — to build AI-native detection that point solutions cannot replicate. Charlotte AI is early, but the data advantage it’s built on is permanent.

Bear Case

Microsoft remains the most dangerous competitor in the market, and its bundle strategy is explicitly designed to make CrowdStrike look expensive. When a CISO can point to Defender, Sentinel, and Entra ID already on the invoice, the CFO conversation becomes very difficult for the CrowdStrike rep — regardless of what the security analysts recommend.

The -20.9% NTM EPS revision in Q1’26 suggests that guidance discipline is either deteriorating or management is sandbagging less aggressively than before. Either way, the Street’s confidence in the forward earnings trajectory is now genuinely impaired, and with a 82x forward P/E, there is no margin of safety if estimates continue to drift downward.

The market for AI-native security startups is not standing still. Emerging competitors with cloud-native architectures and no legacy code debt are building at a speed that CrowdStrike’s engineering team — now managing a massive existing platform — may struggle to match. The moat is real today, but the pace of competitive innovation in cybersecurity is unlike any other sector.

Sea Ltd. (SE)