We get 1Q results from ASML at 1AM ET overnight tonight. This post outlines Consensus expectations for 1Q and forward guidance, the historical valuation context, and our Bull / Bear Bullets overviewing the long and short theses.

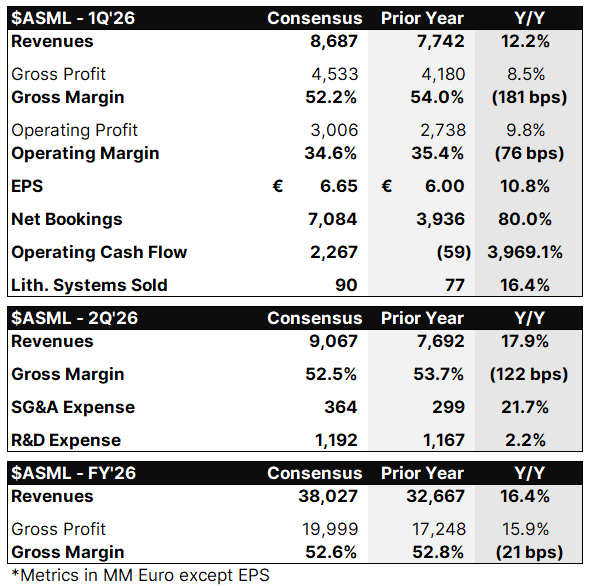

First, Consensus expectations:

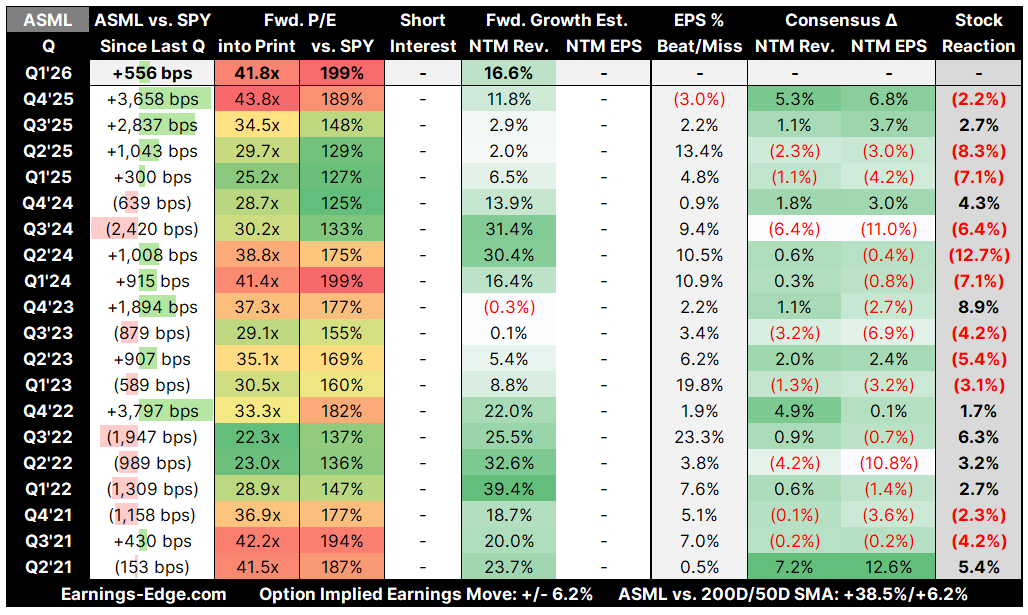

Next, historical valuation context (hot but hot as hot as last Q and with better forward revenue expectations):

And finally, our Bull / Bear Bullets (also found for all reporters of note here):

Bull Bullets: High-NA EUV Ramp, AI-Driven Lithography Intensity, and $34–39B Revenue Guide in Sight

TSMC’s projection that Nvidia product wafer requirements will grow from ~2.5 wafers to ~10 wafers by 2027 illustrates the dramatic increase in lithography intensity driven by AI chip complexity — ASML, as the sole supplier of EUV systems, is uniquely positioned to capture this step-up in demand through increased system shipments and service revenue on its growing installed base.

ASML’s Q4 2025 EUV bookings of €7.4B out of total net bookings of €13.2B demonstrate robust order momentum entering 2026, and management’s 2030 revenue target of €44–60B with 56–60% gross margins implies a multi-year earnings compounding story that the current €34–39B 2026 guide represents only an early chapter of.

The new €12B share buyback program (to be completed by end of 2028) combined with a proposed total dividend of €7.50 per share signals management confidence in free cash flow durability — as interest rate uncertainty subsides and AI capex cycles accelerate, ASML’s cash returns profile could support meaningful multiple expansion.

Bear Bullets: Tariff Uncertainty, Booking Miss, and China Normalization Risk Weigh on Near-Term Outlook

Q1 2025 net bookings of €3.9B missed analyst estimates, and ASML’s CFO explicitly warned that tariff announcements have increased macro uncertainty — with Q2 2026 revenue guidance guided below consensus (€7.2–7.7B vs. €7.73B expected), bookings in the upcoming Q1 2026 report will be the single most watched data point, and another miss could reignite fears that the 2026 growth ramp is slower than modeled.

Global tariffs present a structural cost risk: ASML’s components cross the Atlantic multiple times during manufacturing and assembly, making it unusually exposed to bilateral tariff escalation between Europe and the U.S. — while ASML intends to pass costs to customers, doing so could slow order velocity from cost-sensitive foundry customers.

China revenue is guided to normalize toward ~20% of total sales in 2026 (down from elevated levels in 2024–2025 as customers front-ran export restrictions), and any regulatory tightening of DUV export controls would reduce a meaningful revenue buffer that has been supporting near-term financials.

Key Investment Thesis

ASML is the world’s only manufacturer of extreme ultraviolet (EUV) lithography systems, the critical technology required to produce the most advanced semiconductors used in AI, mobile, and high-performance computing applications.

Upside Case: AI-driven chip complexity continues to increase lithography intensity per wafer, high-NA EUV systems ramp into volume production ahead of schedule, and ASML’s installed base expands toward its 2030 targets — driving a multi-year compounding of both system revenue and high-margin service revenue, with gross margins approaching the 56–60% long-term target range.

Downside Case: Macro uncertainty and tariff-driven cost pass-throughs slow customer investment decisions, China revenues compress faster than anticipated as export controls tighten further, and 2026 bookings disappoint relative to what’s needed to sustain ASML’s growth narrative into 2027–2030.

Differentiation: ASML’s monopoly on EUV technology — protected by decades of R&D investment, proprietary optics from Carl Zeiss, and an ecosystem of 5,000+ supplier relationships — creates an effectively insurmountable competitive moat that no geopolitical or regulatory action is capable of quickly displacing.