Another Squeeze? Previewing Wingstop's Consensus Expectations

Consensus Estimates + Valuation Context

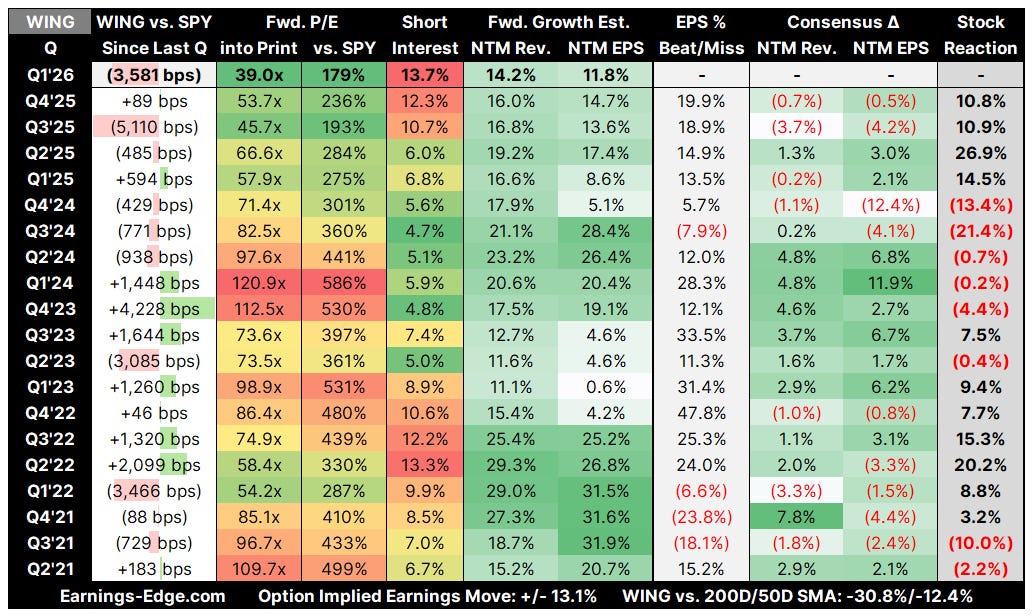

We’ve seen squeezes higher in Wingstop each of the last four quarters despite rather unremarkable financial results.

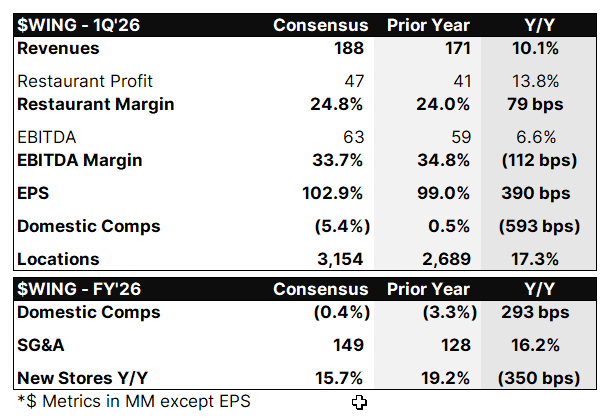

We enter 1Q with a still wholly uninspiring set of expectations (-5% comp sales, declining EBITDA margins), and full year estimates have somehow moved below guidance, notably comp sales ‘flat to +LSD’, now estimated as negative:

Add the squeeze nature to even weak results and a valuation that is the cheapest in history at 39x forward earnings, and the setup looks favorable:

Bull Bullets: Club Wingstop National Launch, International Unit Growth Acceleration, and Deep Valuation Reset

Club Wingstop Loyalty Program National Launch in Q2 2026 Is the Most Important Catalyst in the Company’s History

The Club Wingstop loyalty pilot delivered extraordinary results: nearly 50% of active guests enrolled in test markets, loyalty members increased visit frequency by 7%, and over 30% of new guests joined. The national rollout, targeted for end of Q2 2026, will reach into Wingstop’s 60M+ digital database. Management believes that even small increases in visit frequency could meaningfully advance its goal of reaching $3M average unit volumes (currently $2.0M domestically). For a brand where digital sales already represent 73.2% of system-wide sales, a loyalty program creates a powerful data-and-personalization layer that competitors without comparable digital infrastructure cannot easily replicate. This is the single largest comp sales driver Wingstop has ever deployed, and the timing aligns perfectly with the need to inflect same-store sales back to positive territory.

493 Net New Openings in 2025, 15-16% Global Unit Growth Guided for 2026, and 10,000-Unit Long-Term Target Provides Massive Runway

Wingstop surpassed 3,000 global units in 2025 and entered six new international markets, with India entry targeted for 2026 (potential for 1,000+ units in that market alone). The long-term target of 7,000 global restaurants (4,000 domestic, 3,000 international) means the current footprint is less than half of the total opportunity, and management has expressed ambitions beyond that toward 10,000+ units. The asset-light, 98% franchised model generates high-margin royalty streams with minimal capital requirements, and return on assets of 18.65% reflects the capital efficiency of the franchise structure. With approximately 2,300 restaurant commitments at year-end, the development pipeline provides multi-year visibility into unit growth regardless of near-term comp sales volatility.

Stock Down 50%+ From All-Time Highs, Trading at 37x Forward Earnings With Analyst Targets Implying 50%+ Upside

WING has fallen from its September 2024 high of $387 to roughly $179, a 54% decline driven by same-store sales deceleration. The average analyst target of $275.47 implies 54% upside, and Citi recently upgraded to Buy with a $230 target, arguing that current levels represent an attractive entry point as H2 2026 comparisons ease dramatically. GuruFocus estimates GF Value at $388 (implying the stock is “significantly undervalued”), and Simply Wall St’s most-followed narrative puts fair value at $292. RBC maintained Outperform at $275 even after lowering from $340. With 2026 adjusted EBITDA growth guided at roughly 15% and the loyalty program not yet in the numbers, the current multiple may look expensive on trailing metrics but could prove reasonable if the comp inflection materializes in H2.

Bear Bullets: Severe Same-Store Sales Deterioration, Consumer Softness Risk, and Premium Multiple Under Pressure

Domestic Comps Have Collapsed From +10.1% to -5.8% in Four Quarters, Breaking a 21-Year Growth Streak

The same-store sales trajectory is brutal: Q1 2025 +0.5%, Q2 -1.9%, Q3 -5.6%, Q4 -5.8%, with full-year 2025 at -3.3%. This ended a 21-consecutive-year streak of positive comparable sales growth. For Q1 2026, one analyst projects comps as weak as -6.5%, significantly worse than earlier expectations. Management guided 2026 domestic comps as “flat to low-single-digit growth,” but subsequent analyst revisions have moved the consensus estimate to -2.5% for the full year, with the first half expected to remain deeply negative before easing comparisons provide a tailwind in H2. If the loyalty program fails to move the needle by Q3, the credibility of the comp recovery narrative collapses, and the stock would likely face another significant leg lower.

Consumer Discretionary Spending Weakness and Bone-In Wing Cost Volatility Threaten Unit Economics

The University of Michigan consumer sentiment index sits at 56.6, well below the 80 threshold signaling optimism, suggesting the macro backdrop for restaurant spending remains unfavorable. While bone-in wing costs declined in Q4 2025 (improving company-owned restaurant margins from 77.6% to 75.6% cost of sales), wing costs are inherently volatile, and any upward reversal would squeeze franchisee profitability and suppress new unit development appetite. If franchisees begin to see deteriorating unit economics (current AUV of $2.0M is down from the peak), the 15-16% unit growth guidance could prove aspirational, and development pipeline commitments could slow or be renegotiated.

Even After a 50% Decline, Valuation Remains Elevated vs. Peers and Leaves No Margin for Error

At a P/E of 26.8x trailing earnings and 36.7x forward earnings, Wingstop still carries a significant premium to the restaurant sector average. Morningstar pegs fair value at just $186 and considers the stock overvalued even after the decline. The concentrated menu (wings, fries, sides) limits Wingstop’s ability to reposition if consumer preferences shift, and the company generates the vast majority of its economics from a single protein category. International expansion, while exciting, carries execution risk in untested markets (India, EMEA, Middle East), and the “House of Flavors” experiential format is unproven at scale. If same-store sales remain negative through 2026 and the loyalty launch disappoints, WING could trade toward $130-$150, reflecting a multiple compression scenario where the market re-rates the stock from a hyper-growth compounder to a mature franchise operator.

Key Investment Thesis

Wingstop is one of the world’s fastest-growing restaurant franchisors, operating a 98% franchised, asset-light model with 3,056 locations across 13 countries, specializing in chicken wings with a digitally-led ordering platform (73% digital mix) and industry-leading unit economics.

Upside Case: If the Club Wingstop national loyalty launch drives a measurable frequency lift (even 3-5% comp improvement from the 7% pilot result), easing H2 2026 comparisons allow comps to inflect positive, and international unit growth continues at 15%+ with strong new-market AUVs, WING could re-rate toward $250-$300 as the market recognizes the comp trough and resumes pricing in the 10,000-unit long-term opportunity.

Downside Case: If domestic comps remain negative through Q3/Q4 2026, the loyalty program fails to deliver the frequency gains seen in pilot markets at national scale, consumer spending weakness deepens, and franchisee economics deteriorate, the premium multiple could compress further toward 25x forward earnings, implying a stock price of $130-$150 and validating the Morningstar view that the growth premium has eroded.

Differentiation: Wingstop’s 98% franchised model, 73% digital sales mix, and focused single-protein concept create the highest-margin, most capital-efficient growth engine in the restaurant sector. No competitor operates with comparable digital penetration, unit economics (18.65% ROA), and franchise density in the chicken wing category, giving Wingstop pricing power and brand strength that casual dining and diversified QSR peers cannot match.